Summer is upon us, and traditionally that’s when families pack their bags and get away for a well-deserved vacation. Since this is the first summer travel season in three years that feels like the before times, airlines and airports are bracing for what is expected to be a particularly busy three months.

At least a couple of airlines, in fact, upgraded their second-quarter revenue projections recently, citing higher-than-expected demand. On Thursday, May 26, Southwest Airlines said it expected revenues from April to June to increase 12% to 15% from the same quarter in 2019, up from earlier projections of 8% to 12%. That comes despite higher fuel prices, which should be “more than offset” by increased revenues, according to the company.

Based on current trends, Southwest “expects solid profits and operating margins” in the second quarter and for all of 2022, the Dallas-based carrier said in an investor update.

JetBlue Airways similarly announced that bookings continue to “exceed expectations” and that the carrier may be on track to collect “record” revenues this summer. JetBlue expects “June revenue per available seat mile to be up more than 20%” compared to the same month in 2019.

As you may know, JetBlue is still trying to outbid Frontier Airlines in an effort to acquire rival low-cost carrier Spirit Airlines, even though Spirit has already agreed to merge with Frontier. This should tell you that airlines are scrambling to gobble up as much market share as possible ahead of an anticipated leisure travel boom.

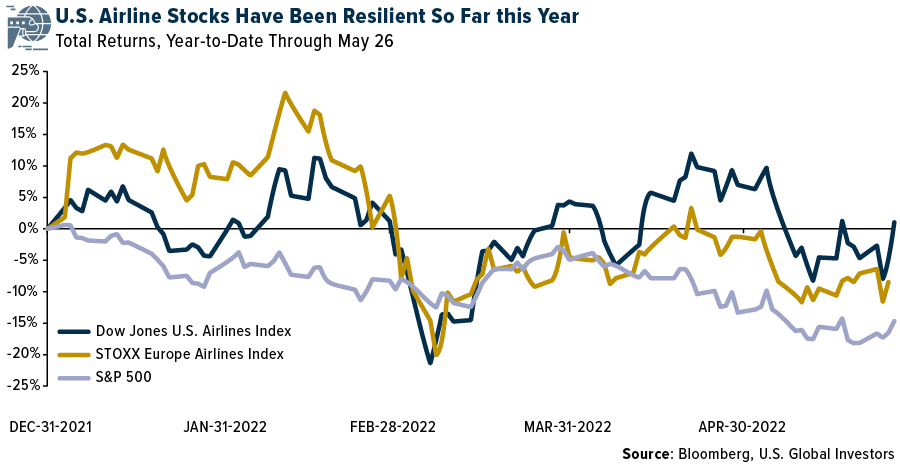

We’re very pleased with how well airline stocks have performed so far this year relative to the market. The Dow Jones U.S. Airlines Index was up more than 3% year-to-date through May 26. Although the STOXX Europe Total Market Airlines Index was down 8% over the same period, that was still ahead of the S&P 500, which has sold off largely on inflation concerns.

That said, below are three airline stocks we’re keeping my eye on as we head into the busy summer leisure travel season.

Southwest Airlines (LUV)

As the original low-cost, no-frills airline, Southwest has had decades’ worth of experience operating at the intersection of comfort and affordability. The company currently has the number one position in 23 of the top 50 markets in the U.S., and the focus right now is on restoring the network to pre-pandemic levels—something that could be achieved by 2023, if not sooner.

Southwest is also focused on maintaining its low-cost advantage. This includes coming up with more efficient flight plans, optimizing maintenance planning and modernizing its revenue management system. In December 2021, the company signed a new credit card co-brand agreement with Chase until 2030, which is already very lucrative. All combined, these initiatives are expected to add between $1.0 billion and $1.5 billion to earnings before interest and taxes (EBIT) by 2023.

Rising jet fuel prices are a concern, but the good news is that Southwest is approximately 64% hedged for the rest of this year at around $60 per barrel. This puts the company in a better position than many of its larger peers that may be unhedged.

Alaska Airlines (ALK)

The more we learn about Alaska, the more we find it attractive. Right now, the company appears to have the best balance sheet in the industry with a 49% debt-to-capitalization ratio. Since the start of the pandemic, Alaska was the first airline to reach no cash burn, the first to become cash flow positive and the first to become profitable.

As the number five U.S. carrier by fleet size and passenger numbers, Alaska is moving toward a low-cost structure that should match Southwest’s by the end of this year or next. The airline has regularly outperformed the domestic industry on operating margin over the past 20 years.

Unlike other airliners, Alaska is working toward having a single-type fleet, which should lead to millions in cost savings in aircraft swaps, maintenance and reduced pilot training. For mainline operations, Alaska will use the Boeing 737, while the Embraer will be used for regional operations. These initiatives are expected to more than offset higher labor costs and airport costs.

Similar to Southwest, Alaska hedges its fuel costs. Half of its fuel requirements are hedged until the end of this year at a cost of $71 per barrel.

In 2016, Alaska merged with Virgin America with the goal of becoming the premiere West Coast carrier. Today its market share in key hubs continues to rise, including in Seattle, Portland, Anchorage, San Francisco and Los Angeles. About 50% of its loyalty participants are in the Pacific Northwest.

Ryanair Holdings (RYAAY)

Now for something a little different, let’s jump across the Atlantic to Ireland, where ultra-low-cost carrier Ryanair is headquartered. The largest airline in Europe, with flights to nearly 40 destination countries, Ryanair is well-positioned to capture an increase in leisure travel demand as Europe drops its Covid-related measures and restrictions.

To give you an idea of just how busy Europe may be this summer, the European airspace manager EUROCONTROL recently said it expects traffic in the upcoming months to stand at 90% of pre-pandemic levels. We believe this could be a huge boon for Ryanair, which reported an average of 2,815 flights per day in April.

Ryanair has been a leader in attracting climate-conscious customers, something that’s increasingly important in the European market. In June of last year, the company took delivery of the Boeing 737-8200 “Gamechanger” aircraft, which purports to reduce fuel consumption by 16% per seat. As of March 2022, Ryanair has taken delivery of 61 of these aircraft and reportedly plans to increase this by an additional 70 within the year.

JETS, the Pure-Play Airlines ETF

The above three airline stocks can be found in the U.S. Global Jets ETF (JETS), a pure-play airline industry exchange-traded fund.

We like to call JETS a smart-beta 2.0 ETF. This means it tracks an index like most ETFs but also shares some characteristics investors might expect to see in an active fund. For instance, JETS is not strictly weighted by market cap weighted, unlike most other ETFs. Instead, it uses a number of quantitative factors to screen for and weight its constituents. It also rebalances and reconstitutes every quarter.

Where will your summer travels take you? Explore the U.S. Global Jets ETF (JETS) by clicking here!

To see the entire list of holdings in JETS, click here.

All opinions expressed and data provided are subject to change without notice. Some of these opinions may not be appropriate to every investor.

Please carefully consider a fund’s investment objectives, risks, charges, and expenses. For this and other important information, obtain a statutory and summary prospectus for JETS by clicking here. Read it carefully before investing.

Investing involves risk, including the possible loss of principal. Shares of any ETF are bought and sold at market price (not NAV), may trade at a discount or premium to NAV and are not individually redeemed from the funds. Brokerage commissions will reduce returns. Because the funds concentrate their investments in specific industries, the funds may be subject to greater risks and fluctuations than a portfolio representing a broader range of industries. The funds are non-diversified, meaning they may concentrate more of their assets in a smaller number of issuers than diversified funds. The funds invest in foreign securities which involve greater volatility and political, economic and currency risks and differences in accounting methods. These risks are greater for investments in emerging markets. The funds may invest in the securities of smaller-capitalization companies, which may be more volatile than funds that invest in larger, more established companies. The performance of the funds may diverge from that of the index. Because the funds may employ a representative sampling strategy and may also invest in securities that are not included in the index, the funds may experience tracking error to a greater extent than funds that seek to replicate an index. The funds are not actively managed and may be affected by a general decline in market segments related to the index. Airline Companies may be adversely affected by a downturn in economic conditions that can result in decreased demand for air travel and may also be significantly affected by changes in fuel prices, labor relations and insurance costs.

Fund holdings and allocations are subject to change at any time. Click to view fund holdings for JETS.

Distributed by Quasar Distributors, LLC. U.S. Global Investors is the investment adviser to JETS.

Revenue per available seat mile (RASM) is a unit of measurement commonly used to compare the efficiency of various airlines. It is obtained by dividing operating income by available seat miles (ASM). In accounting and finance, earnings before interest and taxes is a measure of a firm’s profit that includes all incomes and expenses except interest expenses and income tax expenses. Fuel hedging is a contractual tool some large fuel consuming companies, such as airlines, cruise lines and trucking companies, use to reduce their exposure to volatile and potentially rising fuel costs. The total debt-to-capitalization ratio is a tool that measures the total amount of outstanding company debt as a percentage of the firm’s total capitalization. Cash flow is the total amount of money being transferred into an out of a business, especially as affecting liquidity.

The Dow Jones U.S. Airlines Index measures the performance of the portion of the airline industry which is listed in the U.S. equity market. Component companies primarily provide passenger air transport. Airports and airplane manufacturers are not included. The STOXX Europe Total Market Airlines Index tracks the performance of shares of listed airlines in Europe. The S&P 500 Stock Index is a widely recognized capitalization-weighted index of 500 common stock prices in U.S. companies.