Container shipping companies have not been immune to the disruptive factors roiling markets at the moment, namely rising interest rates, soaring inflation and a potential recession, not to mention war in Eastern Europe.

However, we remain bullish on the global shipping industry for a number of reasons. Below are three charts showing how carriers look to be in positive territory heading into year-end.

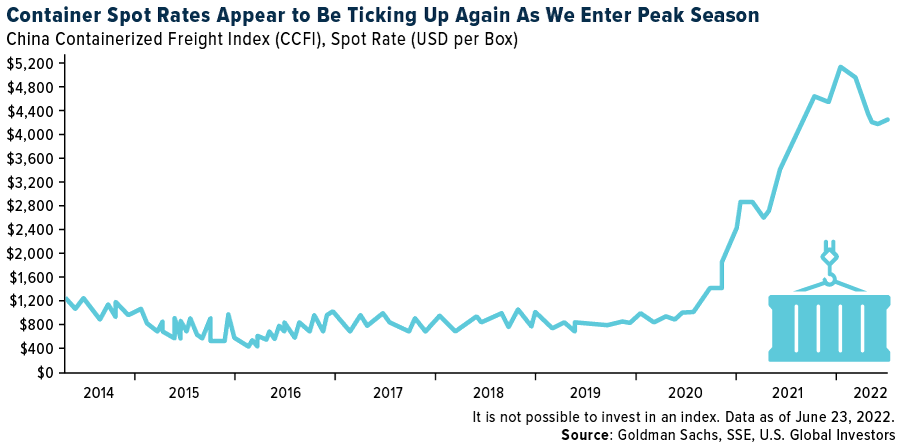

Shipping Rates Remain Highly Elevated on a Historical Basis

The equity research team at Goldman Sachs recently released a report highlighting corporate commentary from its annual conference held in London. Companies across the transport, leisure, construction and business services industries attended, with key takeaways focused on the global transport markets, specifically air travel and shipping.

Below is one of the most compelling charts from the bank’s report. Spot rates for containers leaving major Chinese ports are off their peaks from earlier this year as consumers’ spending habits have shifted from goods to services, but there are two things to keep in mind here. Number one, despite the decline, rates are still highly elevated on a historical basis, which we believe could result in shipping companies posting another profitable year. And number two, it appears that rates may be trying to turn up again as we enter the peak summer shipping season.

Shipping Is a Long-Term Growth Story

Similar to other industries, shipping is seeing higher rates of volatility due to sporadic Covid lockdowns, the conflict in Ukraine, surging inflation and other challenges. As a result, shares of container shipping companies have fallen from their March highs.

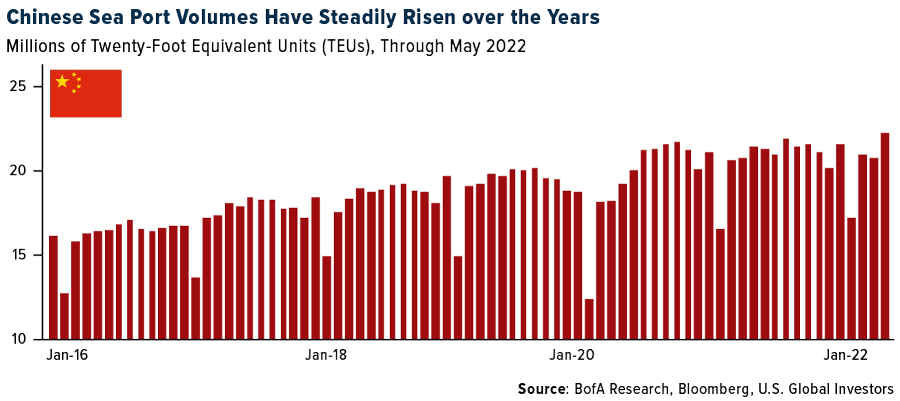

It’s important for investors to keep in mind, though, that shipping is a long-term growth story, particularly in emerging and developing economies. Many countries, most notably in Asia, are undergoing significant economic change as millions of individuals and families join the middle class, a group whose members spend between $11 and $110 a day. According to the World Data Lab, more than 1 billion Asians are expected to join the global middle class by 2030.

We believe this could be constructive news for companies involved in the global shipment of goods. As you can see below, sea port volumes in China have steadily been rising over the years as more and more households have entered the middle class and insisted on buying consumer goods—from furniture to appliances to gadgets—that reflect this socioeconomic change.

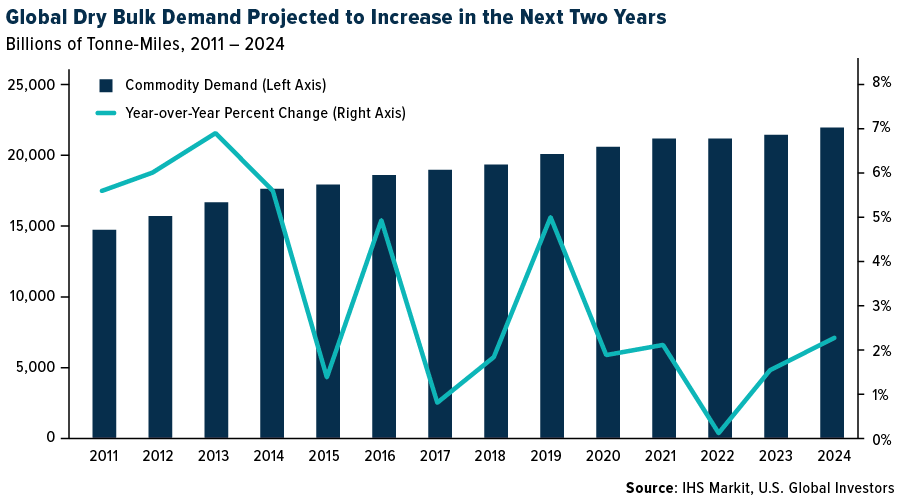

Global Dry Bulk Demand Expected to Increase as Need for Raw Materials Expands

Dry bulk cargo includes the shipment of commodities and raw materials such as iron, steel, wheat, sugar, coal and cement. As the global population continues to expand, the more of these materials will need to be moved across the globe for use in infrastructure, manufacturing, food and other applications. Again, we believe this could benefit companies responsible for carrying dry bulk.

Below is IHS Markit’s dry bulk demand forecast through 2024. Although year-over-year growth is expected to go sideways in 2022 due to sky-high inflation, demand growth could resume in the following two years as prices stabilize.

What this means is now may be a good time to get exposure.

SEA Is a Smart-Beta ETF Based on Quantitative Factors

We believe an ideal way to participate is with the U.S. Global Sea to Sky Cargo ETF (SEA), which provides investors diversified access to the global sea shipping and air freight industries.

Instead of tracking a simple market cap-weighted index, SEA seeks to invest in companies that have exhibited a favorable ability to increase rates, a key driver of revenue growth. Other important factors determining a company’s inclusion in the ETF and its weighting include cash flow return on invested capital, cash flow-to-price and earnings-to-prices.

Think it’s time to set sail? Explore SEA by clicking here!

All opinions expressed and data provided are subject to change without notice. Some of these opinions may not be appropriate to every investor.

Please carefully consider a fund’s investment objectives, risks, charges, and expenses. For this and other important information, obtain a statutory and summary prospectus for SEA by clicking here. Read it carefully before investing.

Investing involves risk, including the possible loss of principal. Shares of any ETF are bought and sold at market price (not NAV), may trade at a discount or premium to NAV and are not individually redeemed from the funds. Brokerage commissions will reduce returns. Because the funds concentrate their investments in specific industries, the funds may be subject to greater risks and fluctuations than a portfolio representing a broader range of industries. The funds are non-diversified, meaning they may concentrate more of their assets in a smaller number of issuers than diversified funds. The funds invest in foreign securities which involve greater volatility and political, economic and currency risks and differences in accounting methods. These risks are greater for investments in emerging markets. The funds may invest in the securities of smaller-capitalization companies, which may be more volatile than funds that invest in larger, more established companies. The performance of the funds may diverge from that of the index. Because the funds may employ a representative sampling strategy and may also invest in securities that are not included in the index, the funds may experience tracking error to a greater extent than funds that seek to replicate an index. The funds are not actively managed and may be affected by a general decline in market segments related to the index. By investing in a specific geographic region, such as China and/or Taiwan, a regional ETFs returns, and share price may be more volatile than those of a less concentrated portfolio. Cargo Companies may be adversely affected by downturn in economic conditions that can result in decreased demand for sea shipping and freight.

The China Containerized Freight Index is the most widely used index for sea freight rates for import China worldwide. This index has been calculated weekly since 2009 and shows the most current freight prices for container transport from the Chinese main ports, including Shanghai. Smart-beta refers to investment strategies that emphasize the use of alternative weighting schemes to traditional market capitalization-based indices.

Fund holdings and allocations are subject to change at any time. Click to view fund holdings for SEA.

Distributed by Quasar Distributors, LLC. U.S. Global Investors is the investment adviser to SEA.