Airlines were one of the hardest-hit industries at the start of the pandemic, with the five-member S&P 500 Passenger Airlines Index collapsing over 31% in 2020. This made the group the worst-performing S&P 500 industry for the year, outside of oil and gas.

The selloff also created an exciting investment opportunity that many young and nontraditional investors, locked down at home and with record disposable income, took advantage of. According to data from Robinhood, the commission-free securities trading platform preferred by millennial and Gen Z investors, distressed airline stocks became one of the year’s breakout hits, with trading volumes hitting historic levels.

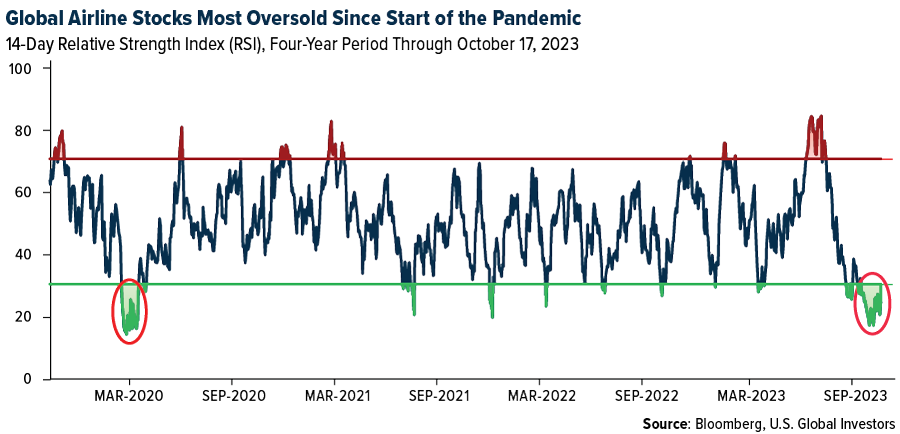

We believe airline stocks appear just as attractive today as they did in 2020. The 14-day relative strength index (RSI) shows that these equities appear more oversold now than at any other time since the pandemic first grounded commercial aircraft. Had you bought shares of global airlines in March 2020, when the RSI fell under 20, you would have seen returns of approximately 130% over the next 12 months.

Will the same happen again this time?

Amid War and Rising Costs, U.S. Air Travel Continues to Soar

It’s important to keep in mind that the causes of both selloffs are vastly different. Whereas commercial air travel across the globe came to a screeching halt in 2020 due to the spread of an as-yet unknown virus, carriers today are grappling with a Middle East at war, spiking fuel prices and persistently high borrowing costs.

United Airlines said as much during its third-quarter earnings call last week. Despite reporting record profits in the quarter ended September 30, shares of United tumbled 9.6% Wednesday, October 18, after it warned shareholders it lowered fourth-quarter projections due to the Israel-Hamas War and oil prices topping $90 per barrel.

Like many other airlines, United has suspended flights to Tel Aviv amid the two-week-old conflict that’s already taken thousands of lives, including approximately 30 American lives. The company said it won’t resume flights to the Israeli city “until conditions allow,” according to reporting by Bloomberg.

The war is certainly a headwind to travel demand, especially if it expands beyond Israel and Gaza’s borders and/or is drawn out longer than anticipated (did anyone expect the skirmish between Russia and Ukraine to still be raging over a year and half later?).

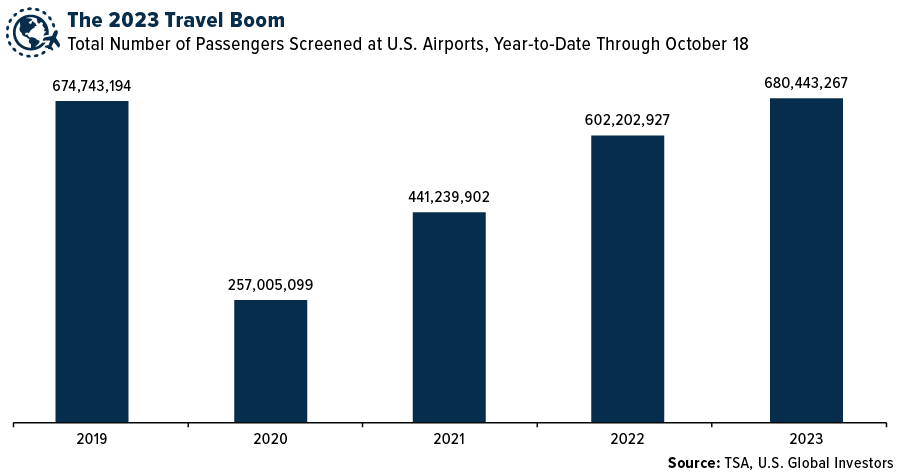

For the time being, however, U.S. consumers don’t appear ready to change their travel habits just yet, even as an overwhelming majority (85%) of Americans say they’re concerned the Israel-Hamas War could escalate to a Middle East-wide engagement, according to a Quinnipiac poll, and even as the State Department issues a “worldwide caution” for U.S. citizens planning to travel overseas. Since October 7, when Hamas attacked Israel, the Transportation Security Administration (TSA) has screened more passengers per day than they did on corresponding days in 2019. So far this year through October 18, millions more people have boarded commercial planes in the U.S. compared to the same period four years ago.

How Airlines Are Leveraging Rewards and Co-Branded Credit Cards

Another reason we like airlines is due to their historical resilience and ability to adapt. This isn’t the first time that the industry has faced and prevailed over a challenging international business climate. Carriers have managed to do this thanks in large part to the implementation of new revenue streams, including loyalty programs and co-branded credit cards.

Co-branded cards have gained a lot of traction in the broader travel sector, airlines specifically. These cards enable consumers to earn loyalty points and other perks, potentially improving customer retention. A couple of examples you might be familiar with are Southwest’s Rapid Rewards and American Express’ Delta Skymiles.

These loyalty programs are big business, accounting for roughly 40% to 50% of airlines’ market value in 2019, according to consultancy firm LTIMindtree. That year, United generated $5.3 billion from the sale of miles, representing a significant portion of its revenue. Delta followed a similar trajectory, selling $4 billion in airline miles to banks, equal to 14% of its operational revenue.

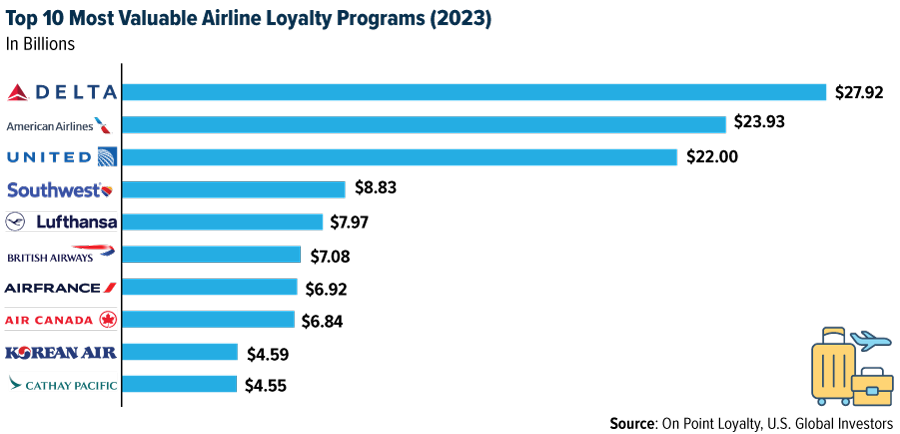

Below are the top 10 most valuable airline loyalty programs in billions of dollars, as of this year. The data comes courtesy of On Point Loyalty, which analyzed 170 commercial passenger airlines, using over 50 primary variables for each program:

As we have pointed out before, ancillary revenue generators such as credit cards and other loyalty programs have become pivotal assets for airlines. With the significant value of these programs now clear, the airline industry is recognizing the vast potential they hold.

If you’re looking to gain access to the global airline industry, check out the full holdings in the U.S. Global Jets ETF (JETS), by clicking here.

To download a copy of the JETS prospectus, fact sheet and investment case, click here.

All opinions expressed and data provided are subject to change without notice. Some of these opinions may not be appropriate to every investor.

Please carefully consider a fund’s investment objectives, risks, charges, and expenses. For this and other important information, obtain a statutory and summary prospectus for JETS by clicking here. Read it carefully before investing.

Investing involves risk, including the possible loss of principal. Shares of any ETF are bought and sold at market price (not NAV), may trade at a discount or premium to NAV and are not individually redeemed from the funds. Brokerage commissions will reduce returns. Because the funds concentrate their investments in specific industries, the funds may be subject to greater risks and fluctuations than a portfolio representing a broader range of industries. The funds are non-diversified, meaning they may concentrate more of their assets in a smaller number of issuers than diversified funds. The funds invest in foreign securities which involve greater volatility and political, economic and currency risks and differences in accounting methods. These risks are greater for investments in emerging markets.

The funds may invest in the securities of smaller-capitalization companies, which may be more volatile than funds that invest in larger, more established companies. The performance of the funds may diverge from that of the index. Because the funds may employ a representative sampling strategy and may also invest in securities that are not included in the index, the funds may experience tracking error to a greater extent than funds that seek to replicate an index. The funds are not actively managed and may be affected by a general decline in market segments related to the index.

Airline Companies may be adversely affected by a downturn in economic conditions that can result in decreased demand for air travel and may also be significantly affected by changes in fuel prices, labor relations and insurance costs.

Fund holdings and allocations are subject to change at any time. Click to view fund holdings for JETS.

Distributed by Quasar Distributors, LLC. U.S. Global Investors is the investment adviser to JETS.

The S&P 500 Airlines Index is a capitalization-weighted index. This is a GICS Level 4 Sub-Industry group. The NYSE Arca Global Airline Index is a modified equal-dollar weighted index designed to measure the performance of highly capitalized and liquid global airline companies.

The Relative Strength Index (RSI) is a momentum indicator that measures the magnitude of recent price changes to analyze overbought or oversold conditions.