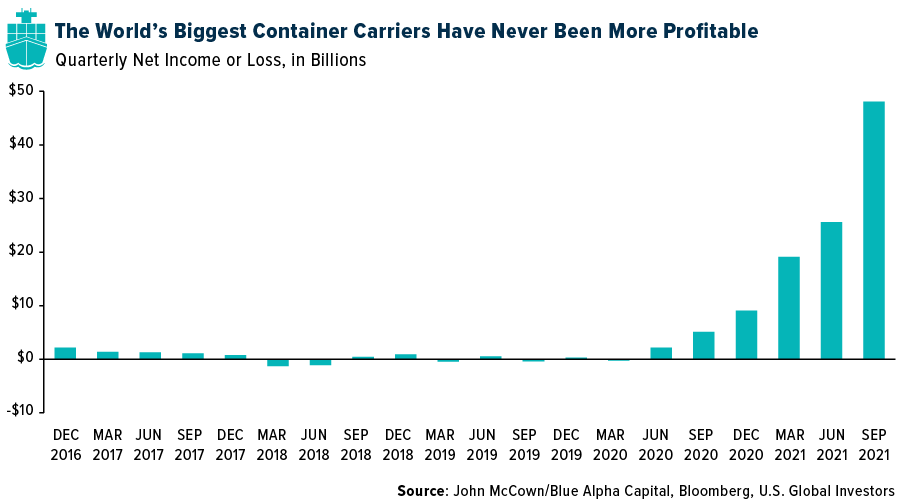

A “boatload” of news this week suggests that the shipping industry continues to look attractive from an investing point of view. For starters, global cargo carriers are estimated to have recorded $150 billion in profits in 2021, the first time they’ve collectively reached that figure in a single year.

Indeed, net income has never been bigger, and it’s not even close. Denmark’s A.P. Moller-Maersk, known simply as Maersk, is expected to report an annual profit that meets or exceeds the combined profits from the past nine years. The world’s second largest carrier, having recently been dethroned by Geneva-based Mediterranean Shipping Company (MSC), sailed up an impressive 72% in 2021 in Copenhagen trading.

To give you an idea of just how cash-flush shipping companies are right now, employees of Chinese state-owned COSCO Shipping, were paid a jaw-dropping year-end bonus that was 30 times their monthly salary, according to Caixin Global. Taiwanese company Evergreen Marine reportedly doled out a bonus that was as high as 40 times workers’ monthly pay.

Rates Likely to Remain Elevated

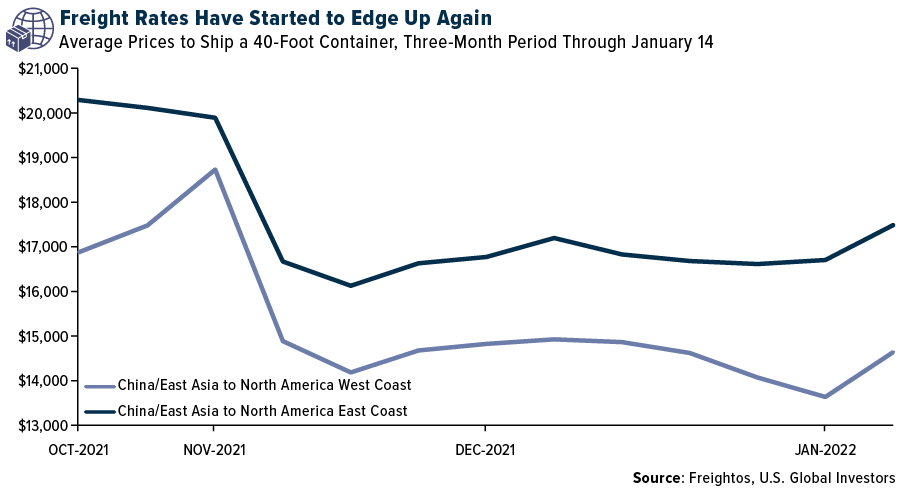

The reason for all of this, of course, is record-high freight rates. Last year, as Covid forced households around the world to shift a lot of their discretionary spending from experiences to goods, the rate to ship a 40-foot container rose to as much as $20,000 in some cases, compared to less than $2,000 in 2019.

Although rates have come off their highs, they’ve lately begun to turn up again as the more transmissible Omicron variant has led to new lockdowns around the world. That includes in China, which CLSA points out has a zero-tolerance approach to controlling the spread of Covid. “Global supply chain pressures are likely to persist, therefore, for much of this year,” CLSA analysts wrote in a note to clients dated January 20.

That thought was echoed by Peter Sand, chief analyst at ocean and air freight benchmarking platform Xeneta. In his weekly update, Sand said he believed that average shipping rates in 2022 “will be higher than ever before,” thanks to companies’ strong pricing power and ability to negotiate long-term rates.

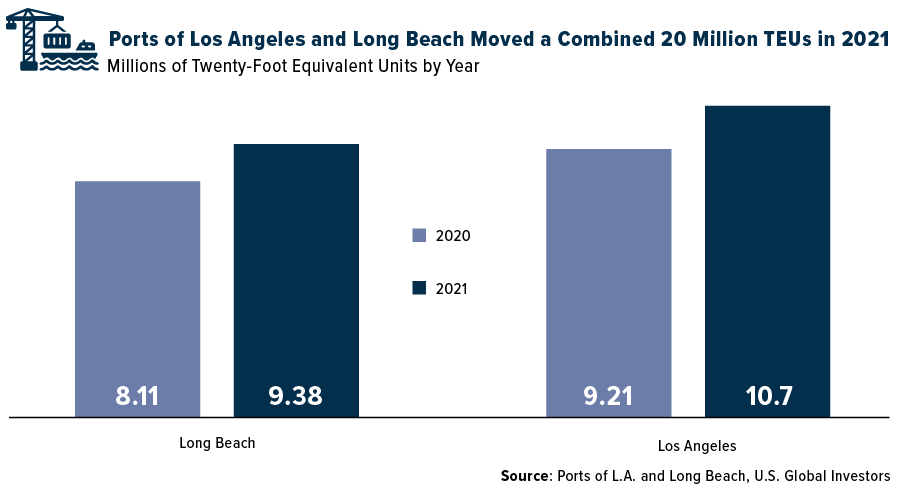

Ports of L.A. and Long Beach Moved a Record Number of Containers

In the past several months, you may have run into some empty store shelves, but it’s not due to a lack of effort. The Ports of Los Angeles and Long Beach released their shipping statistics for calendar year 2021, showing that they’ve never before moved so many containers in a single year. Long Beach handled a record 9.38 million 20-foot equiavlent units (TEUs), a 16% jump in volume from 2020 numbers, while Los Angeles reported moving 10.7 million TEUs, also an increase of 16% from the previous year. Collectively, the two ports, which represent over 25% of North America’s total inbound container trade, handled an unheard-of 20 million TEUs.

It’s not just sea freight, though. Air freight companies had a great 2021. FedEx reported record profit and record revenue of $84 billion last year, largely due to greater volumes. FedEx Express, one of the world’s largest cargo airlines, handled an average of 3.28 million packages per day domestically in 2021, up from 2.90 million packages per day in 2019.

Can Trade Continue to Grow at this Level?

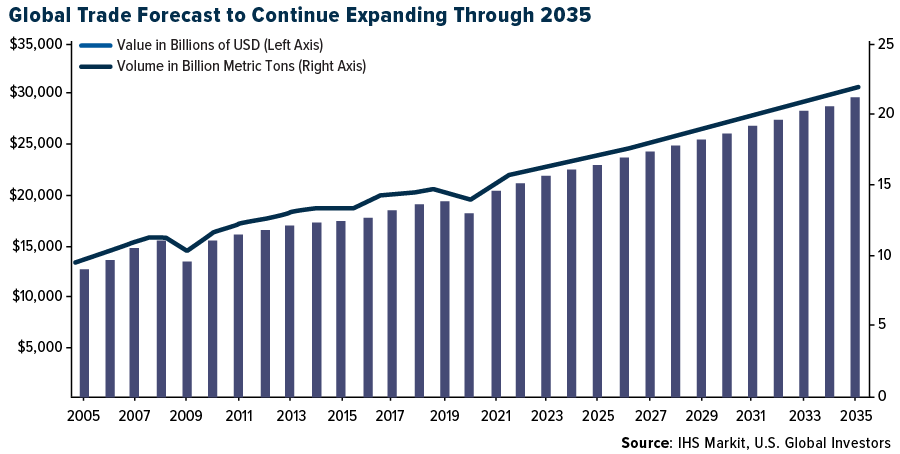

In many ways, last year was an anomaly, and we can’t expect growth in trade volumes to continue at the same high rate indefinitely. But by all accounts, we can reasonably expect them to grow year-over-year as more and more people join the middle class and seek to buy the things associated with such a lifestyle.

According to long-term forecasts by IHS Markit, the real value of traded goods could approach $30 trillion by 2035, up from just over $20 trillion today. Barring another global event like a war, pandemic or economic downturn, volume could exceed 20 billion metric tons, compared to 15.8 billion metric tons today, IHS Markit says.

To be transported all over the world, these future goods will need ships and cargo jets, not to mention ports, a few operators of which are publicly traded. As Americans, we don’t think of airports and seaports as being investable companies, but a few of them are in other countries, including the Philippines’ International Container Terminal Services, New Zealand’s Napier Ports Holding and the U.K.’s PD Ports and Global Ports Holding.

Interested in one way to gain exposure to the global shipping and cargo industries? Explore the U.S. Global Sea to Sky Cargo ETF (SEA), by clicking here!

All opinions expressed and data provided are subject to change without notice. Some of these opinions may not be appropriate to every investor.

Please carefully consider a fund’s investment objectives, risks, charges, and expenses. For this and other important information, obtain a statutory and summary prospectus for SEA by clicking here. Read it carefully before investing.

Investing involves risk, including the possible loss of principal. Shares of any ETF are bought and sold at market price (not NAV), may trade at a discount or premium to NAV and are not individually redeemed from the funds. Brokerage commissions will reduce returns. Because the funds concentrate their investments in specific industries, the funds may be subject to greater risks and fluctuations than a portfolio representing a broader range of industries. The funds are non-diversified, meaning they may concentrate more of their assets in a smaller number of issuers than diversified funds. The funds invest in foreign securities which involve greater volatility and political, economic and currency risks and differences in accounting methods. These risks are greater for investments in emerging markets. The funds may invest in the securities of smaller-capitalization companies, which may be more volatile than funds that invest in larger, more established companies. The performance of the funds may diverge from that of the index. Because the funds may employ a representative sampling strategy and may also invest in securities that are not included in the index, the funds may experience tracking error to a greater extent than funds that seek to replicate an index. The funds are not actively managed and may be affected by a general decline in market segments related to the index. Airline Companies may be adversely affected by a downturn in economic conditions that can result in decreased demand for air travel and may also be significantly affected by changes in fuel prices, labor relations and insurance costs. Gold, precious metals, and precious minerals funds may be susceptible to adverse economic, political or regulatory developments due to concentrating in a single theme. The prices of gold, precious metals, and precious minerals are subject to substantial price fluctuations over short periods of time and may be affected by unpredicted international monetary and political policies. We suggest investing no more than 5% to 10% of your portfolio in these sectors.

Foreign and emerging market investing involves special risks such as currency fluctuation and less public disclosure, as well as economic and political risk. By investing in a specific geographic region, such as China and/or Taiwan, a regional ETFs returns, and share price may be more volatile than those of a less concentrated portfolio.

Cargo Companies may be adversely affected by downturn in economic conditions that csn result in decreased demand for sea shipping and freight.

Fund holdings and allocations are subject to change at any time. Click to view fund holdings for JETS, GOAU and for SEA.

Distributed by Quasar Distributors, LLC. U.S. Global Investors is the investment adviser to JETS, GOAU and SEA.