For those of you who happened to buy a plane ticket in the past month, you may have noticed a welcome change in price. Airfare was down a good amount in June compared to the same month in 2022 (-18.9%) and compared to May (-8.1%), according to last week’s consumer price index (CPI) data. Declining jet fuel costs were the largest contributor to lower fares.

Although this benefits consumers, especially during the busy summer travel months, investors may be wondering: Will airlines generate less revenue as a result? Not so fast.

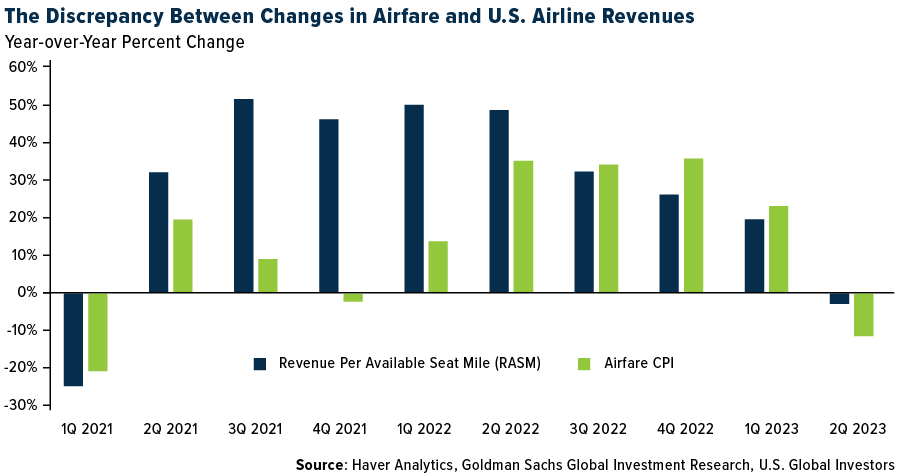

In a letter out last week, Goldman Sachs reports that there doesn’t appear to be a meaningful relationship between airfare CPI and U.S. airlines’ revenue per available seat mile (RASM). Investors, therefore, need not worry—at least not about falling ticket prices.

Check out the chart below. It compares annual percent changes in airfare and airline revenue per seat. Goldman found that there isn’t a strong link between the two, meaning that just because ticket prices are dropping, it doesn’t necessarily mean that carriers are making less money. The bank estimates that second-quarter RASM was off 3% compared to last year’s quarter, but that’s a far cry from how much fares fell during the same period.

Discrepancies Between CPI and RASM in the Airline Industry

So why the discrepancy? The Goldman report doesn’t provide many insights, but we think we can offer a couple.

For one, the Bureau of Labor Statistics (BLS), which issues the monthly CPI, and the airlines are measuring two separate things. The CPI allegedly measures the average change in prices paid by urban consumers for air travel over time. On the other hand, RASM is an airline industry metric that measures an airline’s operating earnings per seat per mile flown—its efficiency, in other words.

The bigger reason for the discrepancy, as we see it, is revenue composition. Airlines make money in many more ways than simply selling tickets. Ancillary revenues, including fees for non-ticket items like extra luggage, seat selection and onboard food, play an increasingly important role in an airline’s total revenue. Baggage fees alone generated a whopping $29 billion for carriers around the world in 2022, according to IdeaWorks.

None of these fees are captured in the airfare CPI, but they surely contribute to RASM.

Other things the CPI appears to get wrong about airfare? It excludes business travel, even though this form of travel involves higher fares than leisure travel due to last-minute bookings, changes, cancellations and added services. The CPI also gathers ticketing data from the Department of Transportation (DOT), which includes only about 10% of tickets sold. Airlines, by comparison, have access to 100% of the data, so they have a much fuller and more accurate understanding of airfare trends.

Delta Reports Record Quarterly Earnings and Profitability

If you need additional proof that lower airfares don’t necessarily impact earnings, look no further than Delta Air Lines. Last week, the carrier reported record earnings and profits in the June quarter on booming travel demand and cheaper fuel, and it gave investors a heads-up to expect another quarter of record revenue in September. Delta raised its 2023 full-year earnings per share (EPS) guidance to between $6 and $7, up substantially from earlier estimates of between $5 and $6 per share.

United Airlines and American Airlines are also forecast to have their best quarterly EPS since 2019.

The earnings boom has helped airline stocks in 2023. Investor’s Business Daily (IBD) said last week that the 19 companies in its Transportation-Airline industry group have increased nearly 50% so far this year, making them the eighth-best-performing industry in 2023 among 197 that the publication tracks.

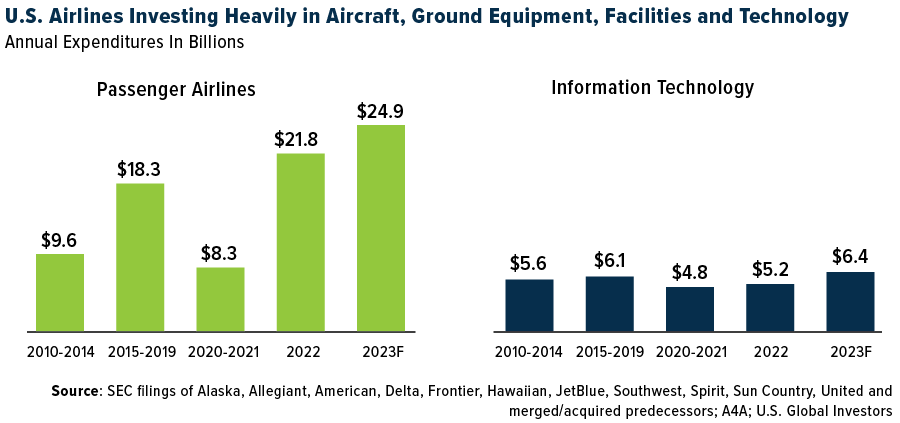

Gearing Up for Growth

Another sign that airlines are bracing for future growth is the incredible amount they’re investing in aircraft, ground equipment, facilities, technologies and other expenditures. In the U.S. alone, airlines are expected to spend nearly $25 billion this year on passenger aircraft and close to $6.5 billion on information technology (IT), which would be a record high in both cases, according to the latest report by Airlines for America (A4A).

In June, Boeing delivered 60 new aircraft, its highest since March, despite lagging behind its European rival Airbus, which delivered 72 aircraft in June, for a total of 316 planes so far this year. Boeing’s notable orders included 40 787 Dreamliners for the new Saudi carrier Riyadh Air, confirmed at last month’s Paris Air Show.

Airbus has a substantial backlog of almost 8,000 aircraft, predominantly single-aisle jets like the A320neo and A321neo. This backlog represents about eight years of production. The manufacturer also booked orders for 902 aircraft, primarily from Air India and IndiGo, accounting for over 70% of its order book.

Meanwhile, here in the U.S., Southwest Airlines plans a $450 million expansion at Houston’s William P. Hobby Airport, adding seven new gates operational by 2026 (six exclusively for Southwest), additional baggage carousels and restroom upgrades. This move facilitates growth in Texas, where Southwest’s Dallas Love Field operations are capped at 20 gates.

To see the full list of holdings in the U.S. Global Jets ETF (JETS), click here.

To download a copy of the JETS prospectus, fact sheet and investment case, click here.

All opinions expressed and data provided are subject to change without notice. Some of these opinions may not be appropriate to every investor.

Please carefully consider a fund’s investment objectives, risks, charges, and expenses. For this and other important information, obtain a statutory and summary prospectus for JETS by clicking here. Read it carefully before investing.

Investing involves risk, including the possible loss of principal. Shares of any ETF are bought and sold at market price (not NAV), may trade at a discount or premium to NAV and are not individually redeemed from the funds. Brokerage commissions will reduce returns. Because the funds concentrate their investments in specific industries, the funds may be subject to greater risks and fluctuations than a portfolio representing a broader range of industries. The funds are non-diversified, meaning they may concentrate more of their assets in a smaller number of issuers than diversified funds. The funds invest in foreign securities which involve greater volatility and political, economic and currency risks and differences in accounting methods. These risks are greater for investments in emerging markets. The funds may invest in the securities of smaller-capitalization companies, which may be more volatile than funds that invest in larger, more established companies. The performance of the funds may diverge from that of the index. Because the funds may employ a representative sampling strategy and may also invest in securities that are not included in the index, the funds may experience tracking error to a greater extent than funds that seek to replicate an index. The funds are not actively managed and may be affected by a general decline in market segments related to the index. Airline Companies may be adversely affected by a downturn in economic conditions that can result in decreased demand for air travel and may also be significantly affected by changes in fuel prices, labor relations and insurance costs.

Fund holdings and allocations are subject to change at any time. Click to view fund holdings for JETS.

Distributed by Quasar Distributors, LLC. U.S. Global Investors is the investment adviser to JETS.

The Consumer Price Index (CPI) is one of the most widely recognized price measures for tracking the price of a market basket of goods and services purchased by individuals. The weights of components are based on consumer spending patterns.