Malcolm McLean may be the most important person you’ve never heard of. His claim to fame? Inventing a box.

But not just any box. McLean—a high school-educated truck driver from North Carolina—came up with the idea of creating a series of standardized, intermodal steel containers that could neatly be stacked on ships as well as trains and trucks.

That was in 1937. It would be another two decades before the first container ship voyage occurred, from Newark to Houston. Ten years after that, in 1966, container shipping expanded to international routes.

Everything changed, though, with the Vietnam War, which created the sudden need for mass volumes of supplies to be transported quickly and efficiently. The shipping container’s time had come. By the end of the 1960s, McLean sold his empire for a profit of $160 million.

According to one estimate, McLean’s invention reduced the cost of shipping by 25%. Some would argue the savings are many times greater than that, perhaps incalculably so.

Just consider labor alone. Before containerization, goods had to be loaded and reloaded by hand at every stop along the supply chain—from ship to port, from port to train, from train to truck. Today, much of this work is seamless and automated.

Below is an excerpt from economist Marc Levinson’s essential history on the container and its impact on our lives, The Box: How the Shipping Container Made the World Smaller and the World Economy Bigger:

“An enormous containership can be loaded with a minute fraction of the labor and time required to handle a small conventional ship half a century ago. A few crew members can manage an oceangoing vessel longer than four football fields. A trucker can deposit a trailer at a customer’s loading dock, hook up another trailer, and drive on immediately, rather than watch his expensive rig stand idle while the contents are removed. All of those changes are consequences of the container revolution.”

The Container Helped Create the Modern Economy

Indeed, few inventions of the past 100 years have touched so many lives as the container. Anyone who makes a purchase on Amazon or steps inside a Costco or other big-box retailer is benefiting directly from McLean’s idea. Anyone who participates at all in the global supply chain—whether they be farmers, fabricators, assemblers or craftsmen—owes a huge debt of gratitude to the container and its ability to facilitate global trade with dependability and at relative low cost.

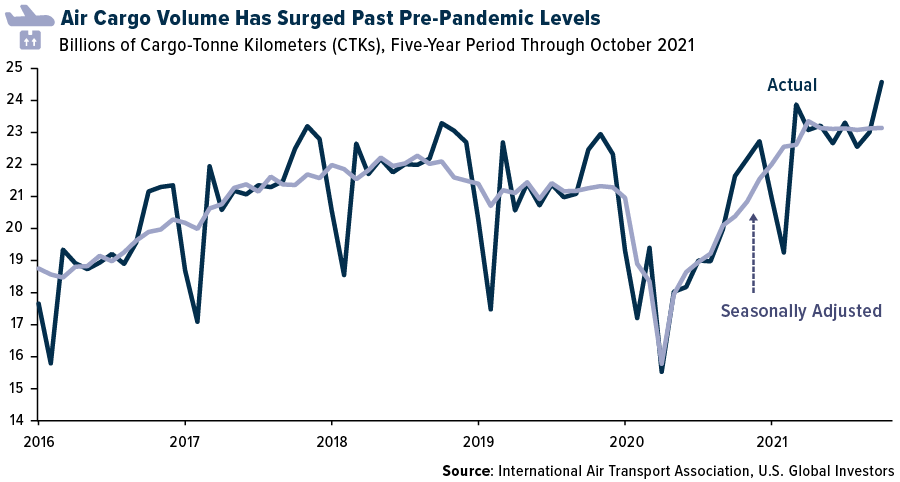

(However, shipping rates, for sea as well as air freight, have soared to new all-time highs since the start of the pandemic. More on that later.)

Between 80% and 90% of global trade is today conducted by sea, with around 60% of that done by maritime container fleets. In 2019, a stunning $14 trillion of all goods worldwide spent some of their time inside the box that was conceived of by a North Carolina truck driver in the 1930s.

The very biggest container ships now can carry approximately 24,000 20-foot containers—compared to only 58 on McLean’s first Newark-to-Houston voyage. (For context, a single 20-footer can carry 18,000 iPads.) The Ever Given, the massive ship that ran aground last year in the Suez Canal, has a carrying capacity of 20,124 20-foot equivalent units (TEUs).

Exercising Capacity Growth Discipline

As you know, shipping rates have surged to all-time highs since the start of the pandemic as households shifted much of their spending from services to goods. Although these sky-high rates have retreated somewhat, shipping companies could potentially be well-positioned to maintain high levels of revenue through capacity growth discipline.

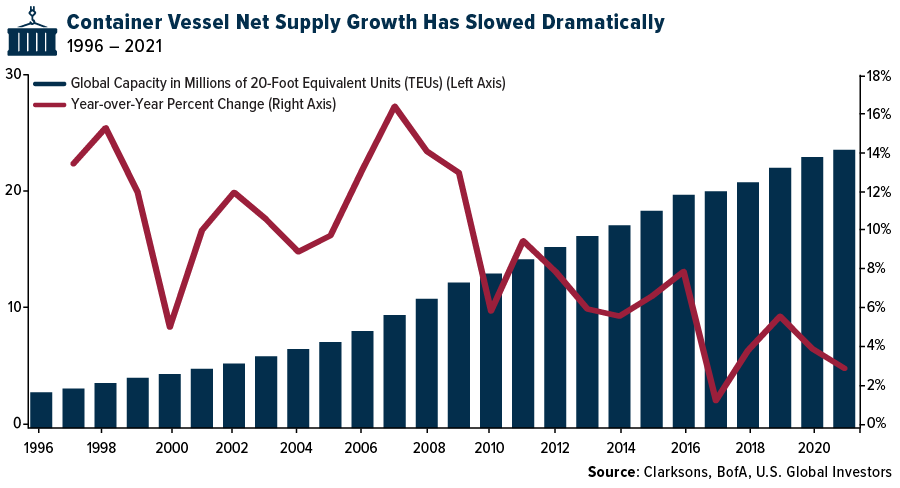

Take a look below. Since at least 1996, global shipping companies have grown the size of their fleets each consecutive year to meet demand, but in the past decade, the rate of expansion has been much lower than in previous years.

There are other ways companies rebalance supply and demand in their favor. One of them is idling, which Bank of America describes as “a relief valve for the industry in order to deal with temporary overcapacity.” Then there’s vessel speed. In recent years, container ships have slowed down, due largely to megaships that have been designed for slower, more fuel-efficient sailing.

And finally, there are scrappings and demolitions. According to BofA, aging vessels become more expensive to maintain and generally have less competitive fuel consumption than newer ships. Scrapping typically slows down, though, during boom periods such as before the financial crisis and in the months since the pandemic began.

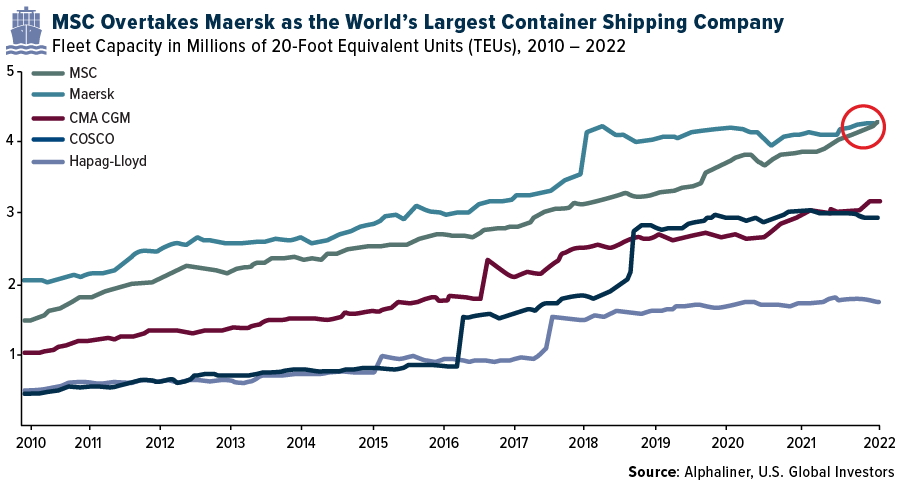

Maersk Dethroned by MSC as World’s Biggest Container Carrier

Remember how McLean sold his company in 1969? The name of that company was SeaLand, which, through a series of subsequent sales and acquisitions, ended up as part of the super-massive Danish shipping conglomerate A.P. Moller-Maersk, today one of the largest companies on the planet with a market cap of about $70 billion.

In its fourth-quarter financial results, released Friday January 14, 2022, Maersk said it generated an incredible $18.5 billion in revenue and earnings before interest, tax, depreciation and amortization (EBITDA) of $8 billion, well above the company’s guidance.

Back in October, Bloomberg analysts estimated that Maersk’s 2021 profits would total $16.2 billion, which would be a record not just for Maersk but any Danish company. We’ll see how accurate this estimate was next month when the company releases its annual report.

In any case, this is important because Maersk has for decades been the largest shipping company by carrying capacity—until recently. Switzerland-based company MSC finally dethroned Maersk recently after it took delivery of several second-hand ships, according to S&P Global. MSC now operates 4.284 million TEUs, compared to Maersk’s 4.282 TEUs.

Interested in one way to gain exposure to the global shipping and cargo industries? Explore the U.S. Global Sea to Sky Cargo ETF (SEA), by clicking here!

All opinions expressed and data provided are subject to change without notice. Some of these opinions may not be appropriate to every investor.

Please carefully consider a fund’s investment objectives, risks, charges, and expenses. For this and other important information, obtain a statutory and summary prospectus for SEA by clicking here. Read it carefully before investing.

Investing involves risk, including the possible loss of principal. Shares of any ETF are bought and sold at market price (not NAV), may trade at a discount or premium to NAV and are not individually redeemed from the funds. Brokerage commissions will reduce returns. Because the funds concentrate their investments in specific industries, the funds may be subject to greater risks and fluctuations than a portfolio representing a broader range of industries. The funds are non-diversified, meaning they may concentrate more of their assets in a smaller number of issuers than diversified funds. The funds invest in foreign securities which involve greater volatility and political, economic and currency risks and differences in accounting methods. These risks are greater for investments in emerging markets. The funds may invest in the securities of smaller-capitalization companies, which may be more volatile than funds that invest in larger, more established companies. The performance of the funds may diverge from that of the index. Because the funds may employ a representative sampling strategy and may also invest in securities that are not included in the index, the funds may experience tracking error to a greater extent than funds that seek to replicate an index. The funds are not actively managed and may be affected by a general decline in market segments related to the index. Airline Companies may be adversely affected by a downturn in economic conditions that can result in decreased demand for air travel and may also be significantly affected by changes in fuel prices, labor relations and insurance costs. Gold, precious metals, and precious minerals funds may be susceptible to adverse economic, political or regulatory developments due to concentrating in a single theme. The prices of gold, precious metals, and precious minerals are subject to substantial price fluctuations over short periods of time and may be affected by unpredicted international monetary and political policies. We suggest investing no more than 5% to 10% of your portfolio in these sectors.

Foreign and emerging market investing involves special risks such as currency fluctuation and less public disclosure, as well as economic and political risk. By investing in a specific geographic region, such as China and/or Taiwan, a regional ETFs returns, and share price may be more volatile than those of a less concentrated portfolio.

Cargo Companies may be adversely affected by downturn in economic conditions that csn result in decreased demand for sea shipping and freight.

Fund holdings and allocations are subject to change at any time. Click to view fund holdings for JETS, GOAU and for SEA.

Distributed by Quasar Distributors, LLC. U.S. Global Investors is the investment adviser to JETS, GOAU and SEA.

EBITDA, or earnings before interest, taxes, depreciation, and amortization, is a measure of a company’s overall financial performance and is used as an alternative to net income in some circumstances.