Will 2023 be the year that gold hits $3,000 an ounce?

Ole Hansen, respected commodity strategist at Denmark’s Saxo Bank, says he thinks it’s possible once markets realize that global inflation will remain hot despite monetary tightening. At U.S. Global Investors, CEO Frank Holmes believes it might have the potential to climb even higher, although of course nothing can be guaranteed.

Hansen notes three other factors that could possibly help push the metal to new record highs next year. One, an increasing “war economy mentality” could discourage central banks from holding foreign exchange reserves in the name of self-reliance, which could favor gold. Two, governments will continue to drive up deficit spending on ambitious projects such as the energy transition. And three, a potential global recession in 2023 might prompt central banks to open the liquidity spouts.

The analyst has already said that his comments are less of a forecast and more of a “thought experiment,” but investors might not want to brush him aside so easily.

Central Banks on a Gold Buying Spree

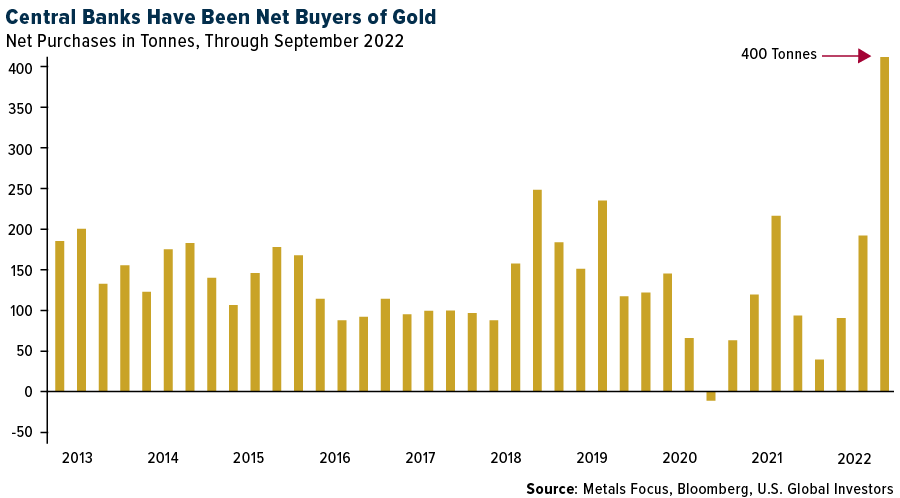

Hansen is correct in bringing up central banks’ increasing appetite for gold as a reserve asset. Central bankers and finance ministers may be all about fiat currency, but behind the scenes, they’re gobbling up the yellow metal at the fastest pace in living memory. In the third quarter, official net gold purchases were approximately 400 tonnes, around $20 billion, the most in over a half-century.

Turkey was the biggest gold buyer in the third quarter, followed by Uzbekistan and India.

Last week, China’s central bank disclosed it purchased gold for the first time since 2019. The Asian country said it recently added 32 tonnes, or $1.8 billion, bringing its total to 1,980 tonnes.

Despite being the sixth largest holder of gold, not counting the International Monetary Fund (IMF), China still has a long way to go if it wants to diversify away from the U.S. dollar in a meaningful way. The metal represents only 3.2% of its total reserves, according to World Gold Council (WGC) data. Compare that to 65.9% of reserves in the U.S., the world’s largest holder with more than 8,133 tonnes.

This is very bullish for the yellow metal, and we might see a lot more buying from China in the coming months.

Over-tightening Risk and Recession Watch

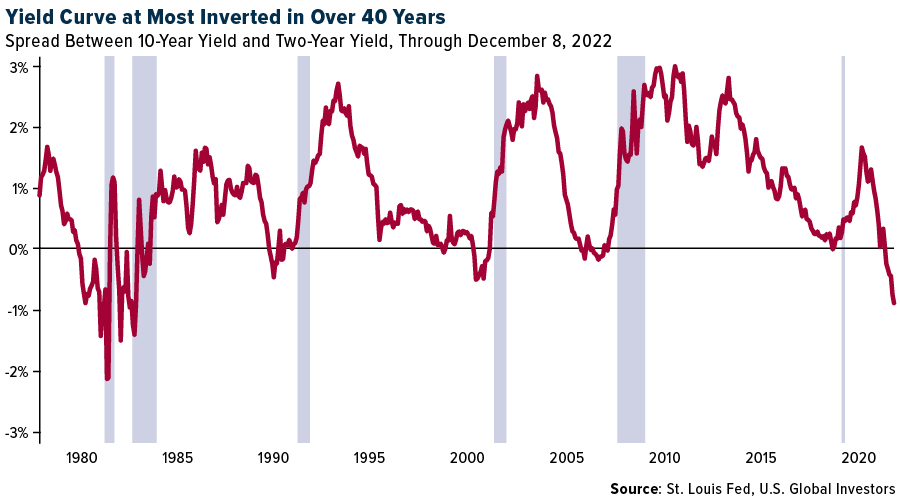

With inflation looking to persist into next year, a small to moderate recession appears to be more and more likely. There’s the risk that the Federal Reserve will overtighten, and this has strong macroeconomic implications for gold.

An indicator we keep our eyes on is the spread between the 10-year Treasury yield and two-year Treasury yield. Over the past 40 years (at least), every recession has been preceded by a yield curve inversion. As of today, the yield curve is at its most inverted in over 40 years, suggesting a recession is all but guaranteed. The question is not if, but when.

In recent days, most banks and ratings agencies have slashed their global growth estimates for 2023 on expectations of persistently high consumer prices and rapid monetary tightening. Buying gold now could possiblyprove itself to be a wise investment choice. In five out of the last seven recessions, gold delivered positive returns, according to the World Gold Council.

Is Gold Setting Up for a Rally?

Technically, gold is starting to look attractive right now, the metal having broken above its 50-day and 200-day moving averages. After breaching the key $1,800-an-ounce level the week before last, gold is again testing the psychologically important price point.

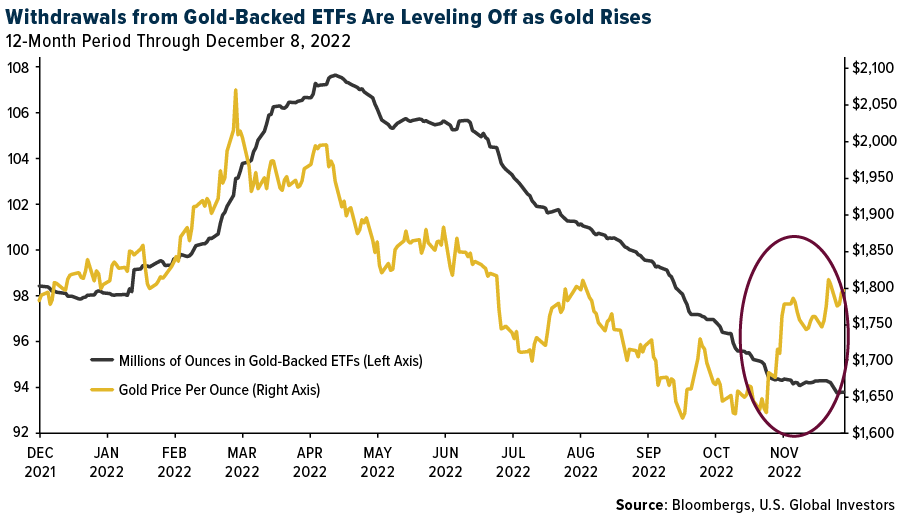

If 2022 ended today, this would mark the second straight year that gold has declined. And yet, at negative 1.75%, the yellow metal has remained one of the best assets to hold this year.

It hasn’t always been easy. Holdings in all known gold-backed gold ETFs have declined for seven months straight as of November 2022. However, we’re starting to see these declines level off as gold begins to push higher.

A gold rally—possibly to $3,000, as Ole Hansen forecasts—would also be highly constructive for gold mining stocks. These companies are much more volatile than the price of the underlying metal. As you can see below, when gold has jumped, gold mining stocks have historically jumped higher. (The reverse has also been true.)

Looking for ways to get exposure to gold and precious metals mining stocks? We’re pleased to offer the U.S. Global GO GOLD and Precious Metal Miners ETF (NYSE: GOAU), which provides investors access to companies engaged in the production of precious metals either through active (mining or production) or passive (owning royalties or production streams) means.

Explore GOAU by clicking here!

PAST PERFORMANCE IS NO GUARANTEE OF FUTURE RESULTS.

All opinions expressed and data provided are subject to change without notice. Some of these opinions may not be appropriate to every investor.

Please carefully consider a fund’s investment objectives, risks, charges, and expenses. For this and other important information, obtain a statutory and summary prospectus for GOAU here. Read it carefully before investing.

Investing involves risk, including the possible loss of principal. Shares of any ETF are bought and sold at market price (not NAV), may trade at a discount or premium to NAV and are not individually redeemed from the funds. Brokerage commissions will reduce returns.

Because the funds concentrate their investments in specific industries, the funds may be subject to greater risks and fluctuations than a portfolio representing a broader range of industries. The funds are non-diversified, meaning they may concentrate more of their assets in a smaller number of issuers than diversified funds.

The funds invest in foreign securities which involve greater volatility and political, economic and currency risks and differences in accounting methods. These risks are greater for investments in emerging markets. The funds may invest in the securities of smaller-capitalization companies, which may be more volatile than funds that invest in larger, more established companies.

The performance of the funds may diverge from that of the index. Because the funds may employ a representative sampling strategy and may also invest in securities that are not included in the index, the funds may experience tracking error to a greater extent than funds that seek to replicate an index.

The funds are not actively managed and may be affected by a general decline in market segments related to the index. Gold, precious metals, and precious minerals funds may be susceptible to adverse economic, political, or regulatory developments due to concentrating in a single theme. The prices of gold, precious metals, and precious minerals are subject to substantial price fluctuations over short periods of time and may be affected by unpredicted international monetary and political policies. We suggest investing no more than 5% to 10% of your portfolio in these sectors.

Fund holdings and allocations are subject to change at any time. Click to view fund holdings for GOAU.

Distributed by Quasar Distributors, LLC. U.S. Global Investors is the investment adviser to GOAU.

The Philadelphia Stock Exchange Gold and Silver Index is a capitalization-weighted index which includes the leading companies involved in the mining of gold and silver.

One cannot invest directly in an index.

All opinions expressed and data provided are subject to change without notice. Some of these opinions may not be appropriate to every investor.