Gold mining stocks appear very unloved at the moment. As measured by the NYSE Arca Gold Miners Index, gold equities fell 18.5% year-to-date through the end of July, underperforming both the underlying metal and the S&P 500. From the index’s recent high set in August 2020, gold miners are off about 42.5%, putting them deep in bear territory.

When an asset class gets to be this overlooked by investors, we believe the time becomes ripe for contrarians to consider making a move.

There’s more to the investment case than market timing. Systemic risks abound right now that, in our view, could favor allocations to physical gold and gold mining stocks. Those risks include sustained inflation, a potential global recession, looming food and energy crisis, and an escalation of hostilities in Eastern Europe.

Reining in inflation alone will be no small task. The historic jump in consumer prices was likely years in the making due to unrestrained money-printing by central banks around the world, coupled with significant supply chain disruptions stemming from pandemic-related lockdowns. Besides aggressive rate hikes, austerity may need to be implemented to mute demand.

Historical Parallels

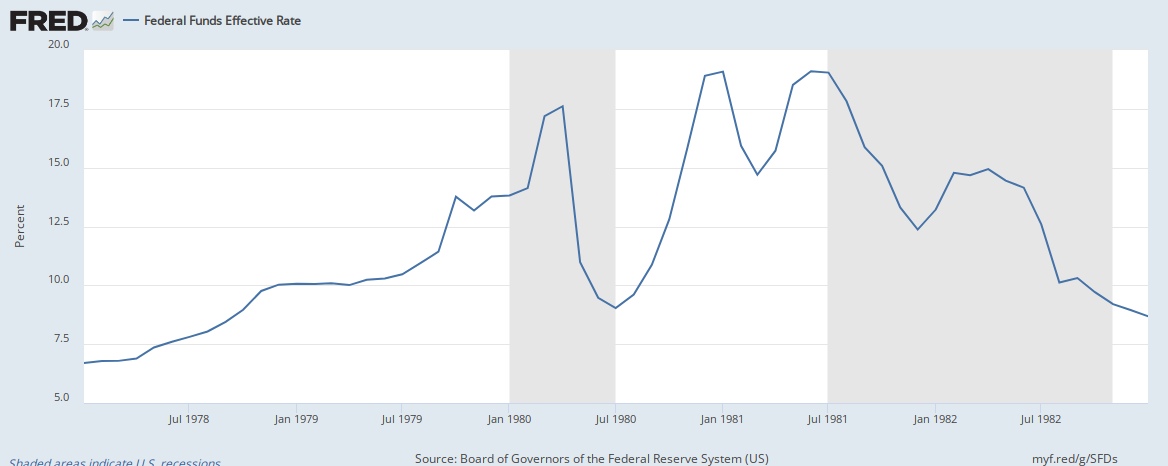

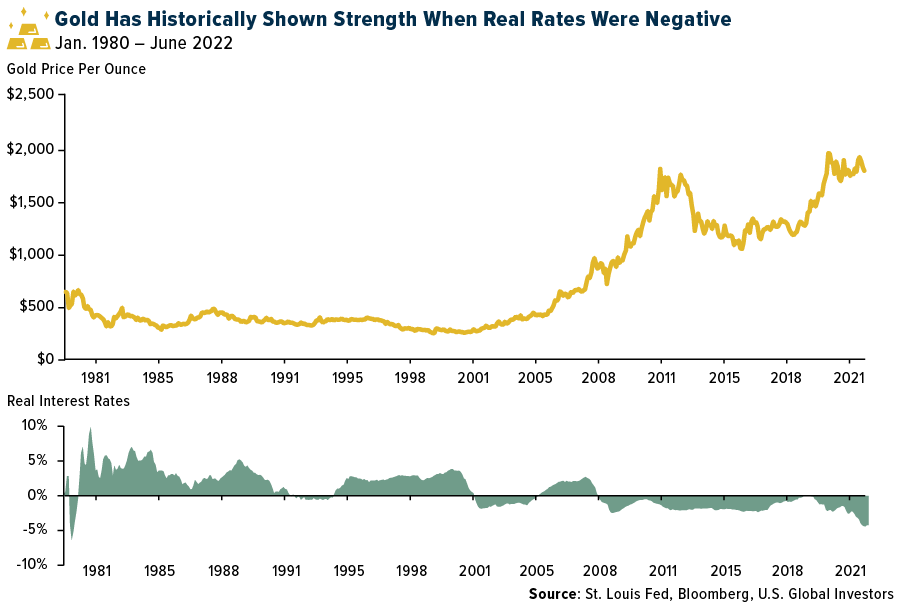

It’s worth pointing out that the last time we saw inflation this hot was in the early 1980s. This prompted similarly aggressive action by then-Federal Reserve Chair Paul Volcker, who raised rates to as high as 19%, according to Fed data. Gold responded by soaring to $850 an ounce on January 21, 1980, which is more than $3,000 in today’s dollars, an all-time high when adjusted for inflation.

{kind=link}

Gold often shares an inverse relationship with real rates. When inflation-adjusted rates have turned negative, the precious metal has tended to trade up as investors dumped government bonds in favor of gold and other hard assets.

Today, real interest rates are as negative as they were in 1980, but so far, the gold price has remained below $1,800, some distance from its nominal high of $2,073 an ounce, set in August 2020, and its inflation-adjusted high of around $3,000.

Strong Dollar Has Contained Gold

The reason we believe we haven’t seen gold rip to a new all-time high this year in light of systemic risks is the strong U.S. dollar compared to other world currencies. Like most other commodities, gold is priced in dollars, so when the value of the greenback is high, it has the effect of containing the metal’s price.

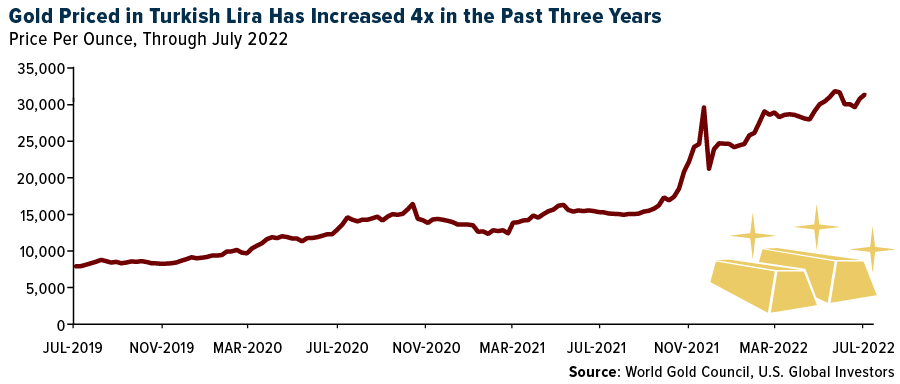

Year-to-date through the end of July, the only major currencies to have increased in value relative to the dollar are the Russian ruble and Brazilian real. Most currencies have decreased in value, with the Turkish lira having lost a little over a quarter of its value compared to the greenback.

Below are the results. While dollar-denominated gold has been stuck in a tight range, gold priced in the Turkish lira has exploded. Over the past three years through the end of July, the gold price in Turkey has increased fourfold and is currently trading near an all-time high, underlining the metal’s perceived role as a hedge against monetary debasement.

A Contrarian Play

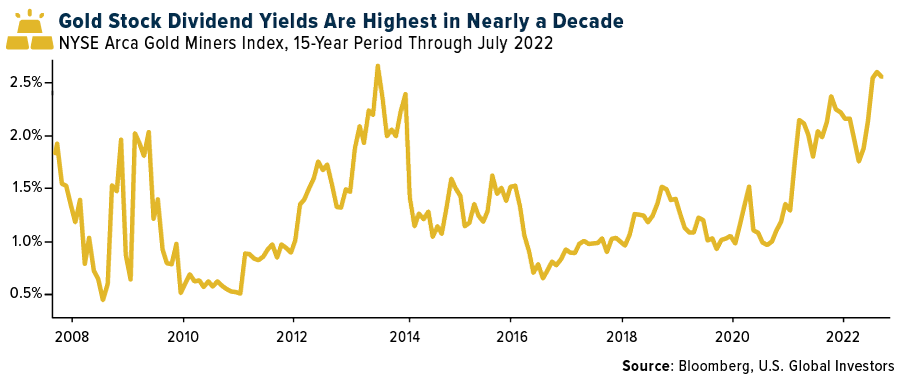

As for precious metal miners, we see them as an attractive opportunity right now. They’re trading at a huge discount compared to the broader equity market, and dividend yields are the highest they’ve been in nearly a decade.

What we believe could benefit miners is a potential pivot by Jerome Powell and the Fed. We’re currently in a tightening cycle, with another 50- to 75-basis point rate hike expected in September. But as soon as the central bank is convinced that inflation has come under control, policy may rapidly shift back to being accommodative to prevent an even deeper economic slowdown. For such a capital-intensive, highly leveraged industry as mining is, that would be welcome news.

We’re pleased to offer the U.S. Global GO GOLD and Precious Metal Miners ETF (NYSE: GOAU), which provides investors access to companies engaged in the production of precious metals either through active (mining or production) or passive (owning royalties or production streams) means.

To learn more about GOAU and download the prospectus, fact sheet and investment case, click here.

PAST PERFORMANCE IS NO GUARANTEE OF FUTURE RESULTS.

All opinions expressed and data provided are subject to change without notice. Some of these opinions may not be appropriate to every investor.

Please carefully consider a fund’s investment objectives, risks, charges, and expenses. For this and other important information, obtain a statutory and summary prospectus for GOAU here. Read it carefully before investing.

Investing involves risk, including the possible loss of principal. Shares of any ETF are bought and sold at market price (not NAV), may trade at a discount or premium to NAV and are not individually redeemed from the funds. Brokerage commissions will reduce returns.

Because the funds concentrate their investments in specific industries, the funds may be subject to greater risks and fluctuations than a portfolio representing a broader range of industries. The funds are non-diversified, meaning they may concentrate more of their assets in a smaller number of issuers than diversified funds.

The funds invest in foreign securities which involve greater volatility and political, economic and currency risks and differences in accounting methods. These risks are greater for investments in emerging markets. The funds may invest in the securities of smaller-capitalization companies, which may be more volatile than funds that invest in larger, more established companies.

The performance of the funds may diverge from that of the index. Because the funds may employ a representative sampling strategy and may also invest in securities that are not included in the index, the funds may experience tracking error to a greater extent than funds that seek to replicate an index.

The funds are not actively managed and may be affected by a general decline in market segments related to the index. Gold, precious metals, and precious minerals funds may be susceptible to adverse economic, political, or regulatory developments due to concentrating in a single theme. The prices of gold, precious metals, and precious minerals are subject to substantial price fluctuations over short periods of time and may be affected by unpredicted international monetary and political policies. We suggest investing no more than 5% to 10% of your portfolio in these sectors.

Fund holdings and allocations are subject to change at any time. Click to view fund holdings for GOAU.

Distributed by Quasar Distributors, LLC. U.S. Global Investors is the investment adviser to GOAU.

The NYSE Arca Gold Miners Index is a rules-based index designed to measure the performance of highly capitalized companies in the Gold Mining industry. The real interest rate is an interest rate that has been adjusted for inflation to reflect the real cost of funds to a borrower. Dividend yield is a financial ratio that tells you the percentage of a company’s share price that it pays out in dividends each year. A basis point is one hundredth of 1 percentage point (.01%).

Investors cannot invest directly in an index.